Key takeaways

- China’s GDP growth target for 2024 of “around 5%” signals a more proactive policy stance.

- The size of the fiscal bill for 2024 is on par with what was delivered in 2023…

- …which may fuel monetary easing expectations; more measures to attract foreign investment will be in place.

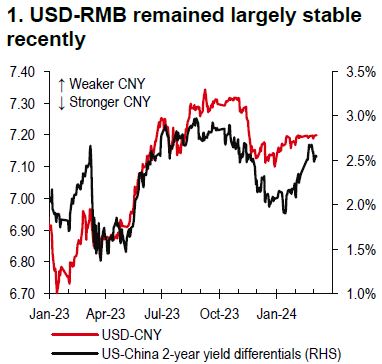

USD-RMB has remained stable (Chart 1), as Chinese Premier Li delivered the Government Work Report at the opening session of the 2024 National People’s Congress (NPC).

China’s 2024 growth target of “around 5%” comes along with fiscal support

The Chinese government has set the 2024 GDP growth target at “around 5%”, matching last year’s goal, albeit above our economists’ expectations of 4.9% and Bloomberg consensus of 4.6%. Market participants naturally expect this meaningful fiscal impulse to drive growth, while the size of the fiscal bill is on par with what was delivered last year. The official fiscal deficit is planned to be 3% (vs an actual fiscal deficit of 3.8% in 2023), alongside RMB1trn worth of ultra-long special government bonds and RMB3.9trn worth of local government special-purpose bonds.

Monetary policy is likely to remain accommodative

Without more expansionary fiscal policy, the People’s Bank of China (PBoC) will need to continue its efforts to balance monetary easing while maintaining FX stability. China’s long-term government bond yields have fallen quickly after a 50bp reduction in the banks’ reserve requirement ratio (RRR) and a 25bp cut to its 5-year loan prime rate (LPR) earlier this year. The relatively conservative fiscal budget announced at the NPC may further fuel policy rate cut expectations. A stable FX policy will be needed to offset persistent outflow pressures, amid wide US-China yield differentials (Chart 1), amongst other considerations.

More measures to attract foreign investment will be in place

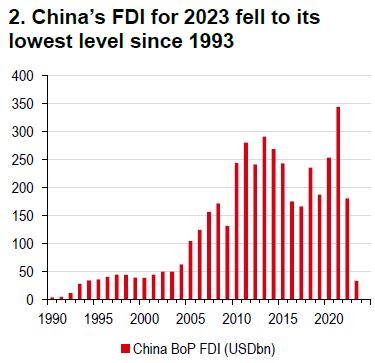

In the Government Work Report 2024, the Chinese government has also committed to implementing other measures to attract foreign investment inflows. In particular, it calls for the scrapping of all restrictions on foreign investment in the manufacturing sector, while relaxing market access to services sectors. These measures aim to level the playing field for state-owned enterprises (SOEs), private-owned enterprises (POEs), and foreign enterprises. If implemented swiftly, it could help improve the business environment and improve sentiment, in our economists’ view. The latest balance of payments (BoP) data suggests that foreign direct investment (FDI) fell to USD33bn last year, the lowest level in China since 1993 (Chart 2).