Key takeaways

- The GBP is the second best performing G10 currency so far this year…

- …in part, due to the considerable hawkish reappraisal of the BoE’s likely policy path.

- As the BoE catches up on the dovish side with other central banks, the GBP could face more downward pressure.

The GBP has performed strongly so far this year…

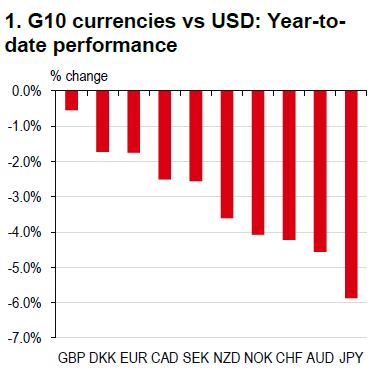

For an economy that is in a technical recession (i.e., two consecutive quarters of negative growth in real GDP), the fact that the GBP is the second best performing G10 currency so far this year (Chart 1) could be viewed as remarkable.

Note: Data was updated on 29 February 2024 at 17:30 HKT.

…as the path to a full dovish pivot by the BoE has been lengthened

In part, this reflects the recent considerable hawkish reappraisal of the Bank of England’s (BoE) likely policy path. So far in 2024, rates markets have taken close to 100bp of easing out of its expected path for the BoE’s policy rate and are now expecting the BoE to start cutting rates in August (Bloomberg, 29 February 2024), which is also our economists’ expectation. While there has also been a hawkish adjustment in the US, it has not been so large.

The GBP is likely to track sideways over the near term amid mixed UK data, in our view

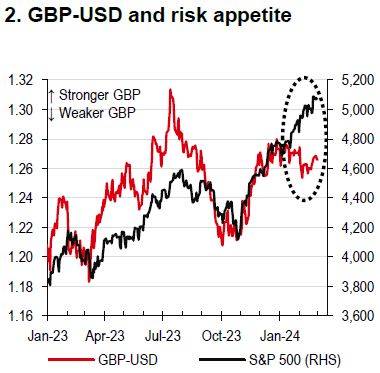

GBP-USD is beholden to rates, and its previous relationship with risk appetite appears to be broken so far this year (Chart 2). As such, the GBP can no longer capitalise on the upside to risk appetite from the US economy’s resilience. However, by the same token, it should mean the GBP is less vulnerable, should there be a measured correction in global risk appetite. All this points to a range-bound GBPUSD over the near term.

We see the GBP facing downside risks in the months ahead

We think that the main driver of the likely weakness for the GBP is the slow but clear pivot by the BoE towards a more dovish stance. The UK still faces a challenging inflation-growth mix, making it hard for the BoE to remain a more hawkish outlier in the G10 space. As the BoE catches up on the dovish side with other central banks, the GBP could face more downward pressure in the months ahead.